How financial markets work

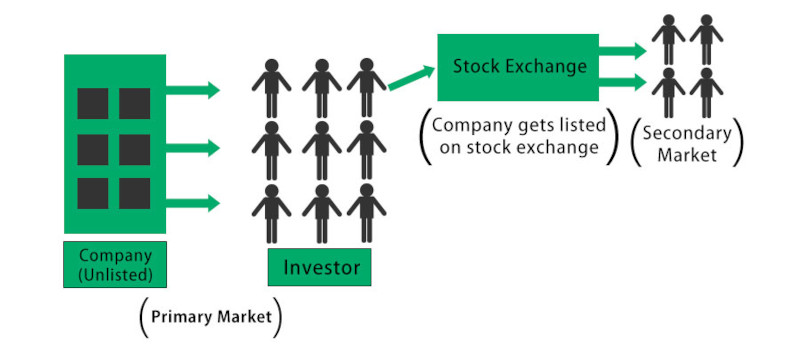

An initial public offering (IPO) is a public offer where the shares of a company are sold to the general public, on a stock exchange, for the very first time. Through this process, a private company is transformed into a public company. Initial public offerings are used by companies to raise expansion capital, to monetise investments from early private investors and to become publicly traded companies.

A company that issues shares is never required to return the capital to its public investors. After the IPO, when stocks are traded freely in the open market, money passes between public investors.

When a company lists its securities on the stock exchange, the money paid by investors for the newly issued shares goes directly to the company (primary offering) as well as to any initial private investor who chooses to sell all or part of his holdings (secondary offer) in the context of the initial public offering. An IPO therefore allows a company to tap into a large pool of potential investors to raise capital for future growth, to repay debts or to obtain working capital.

While IPOs have many advantages, they also have significant disadvantages. The main ones are the costs associated with the process and the obligation to disclose certain information that could be used by competitors or lead to difficulties with sellers. Details of the proposed offer are communicated to potential buyers in the form of a long document known as a "prospectus".

Most companies that go public do so with the help of an investment bank, which acts as an underwriter. Underwriters provide a valuable service, which includes helping to properly assess the value of shares (share price) and establishing a public market for shares (the initial sale).

Offers on the secondary market

A secondary market offer is a registered offer of a large block of shares that had previously been issued to the public. The offered blocks may have been held by large investors or institutions, and the proceeds of the sale go to those holders, not the issuing company. This is sometimes also called secondary distribution.

A secondary offer is not dilutive for existing shareholders, since no new shares are created. The proceeds from the sale of the shares do not benefit the issuing company in any way. The offered shares are held privately by the shareholders of the issuing company, who may be directors or other insiders (such as venture capitalists) who simply want to diversify their holdings. However, the increase in the number of shares available generally allows a greater number of institutions to take significant positions in the issuing company, which can promote the liquidity of the issuing company's shares.

Transactions on the secondary market

After the initial issuance, investors can buy from other investors in the secondary market. In the secondary market, shares are sold and transferred from one investor or trader to another. It is therefore important that the secondary market be very liquid. As a general rule, the more investors who participate in a given market and the more centralised that market, the more liquid it is.

Private placements

Private placements (or non-public offerings) are a round of capital-raising stocks that are not sold through a public offering, but rather through a private offering, primarily to a small number of selected investors. The term "private placement" generally refers to the non-public offering of shares of a public company (since, of course, any offering of shares of a private company is and can be only a private offering).

Share buyback

Share buybacks allow a company to buy back their own shares. In some jurisdictions (UK, USA, etc.), a company can buy back its own shares by distributing cash to its shareholders; that is, cash is paid out in order to reduce the number of outstanding shares. The company can either withdraw the repurchased shares or keep them aside for possible reissue at a later point in time.

Profitable companies generally have two uses for the profits they generate. First, part of the profits can be distributed to shareholders as dividends or via share buybacks. The remaining cash, called equity, is kept within the company and used to invest (R&D, product or service development, new equipment, etc.). If companies can reinvest most of their retained earnings profitably, they will. However, sometimes companies find that some or all of their retained earnings cannot be reinvested to produce acceptable returns.

Recommended stock broker

| Brokers | |

|---|---|

| Account type | Stock trading account, margin account (79% of CFD accounts lose money) |

| Management by mandate | No |

| Stock brokerage fees | No commissions for a min. monthly volume of €100,000 EUR, otherwise 0,20%. |

| Demo account | Yes |

| Our opinion | Trading without commissions, but with a very limited choice of 2,000 shares and 16 ETFs. |

| Broker review | XTB |

| |

Investing carries risks of loss | |