Trading "vanilla" options

The standard call and put options (also called vanilla options) that are found on the major exchanges are different from exotic and binary options.

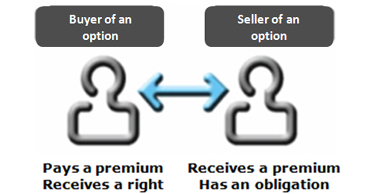

Buying and selling a vanilla option

An investor who buys a call option buys the right to buy a specific amount of an underlying security at an agreed upon strike price (the strike price is the price at which a contract may be exercised until the expiration date), if he buys a put option, he buys the right to sell the underlying security before or upon expiration.

An investor who sells a call option or who emits an option is obligated to comply with the contract's clauses. If he sells a call (an option to buy), he will have to sell the underlying security at the strike price. If he sells a put (a an option to sell), he will have to buy the underlying security at the strike price. The contract can be exercised by the buyer at any time up to the maturity date, the option's issuer or seller therefore has no control. However, if the buyer decides to not exercise his option, and instead prefers to sell it at the going market rate, the issuer can buy the contract back to cancel his obligations and close the transaction.

There are two types of options

- American options: the option can be exercised at any time until expiration.

- European options: the option can only be exercised at expiration.

American-type options tend to be more expensive than European-type options, because they offer more possibilities. Almost all of the stock options traded on the market are American-type. Index options can be issued either as American-type options or European-type options.

The premium of a vanilla option

The buyer of an option pays a premium, but the profit potential is unlimited.

The seller of an option earns a premium, but the potential for loss is unlimited.

The price of an option is limited to the premium. Options therefore offer a significant leverage effect, in the below example the investor pays a 200-euro premium even though the price of 100 shares at 20 euros is 2000 euros.

Example of a vanilla option transaction (CALL)

- Option to buy (CALL) of a share of XX (American-type option)

- Amount: 100 shares of XX

- Expiration date: 30/08/2013

- Exercise price (Strike): 20 euros

- Premium: 2 euros per share

The buyer

In this case, the buyer of a call option pays the premium (2€ * 100 shares) in exchange for the right to buy when he wants up until 30/08/2013, 100 shares of XX at an exercise price (Strike price) of 20 euros per share.

During the life of the option, there are three possibilities:

![]() The price of the share falls down to 15€: the option is "out-of-the-money", the buyer has no reason to exercise his right, he loses the premium (100 * 2€ = 200€).

The price of the share falls down to 15€: the option is "out-of-the-money", the buyer has no reason to exercise his right, he loses the premium (100 * 2€ = 200€).

![]() The price of the share remains at 20€, the option is "at-the-money", the buyer loses the premium (100*2€ = 200€).

The price of the share remains at 20€, the option is "at-the-money", the buyer loses the premium (100*2€ = 200€).

![]() The price of the share climbs to 25€, the option is "in-the-money", the buyer makes a profit from which he must deduct the premium (100*25€ - 100*20€) - (premium 200€) = 300€ profit. He can sell his call to close his position or exercise the option to buy 100 shares at 20€.

The price of the share climbs to 25€, the option is "in-the-money", the buyer makes a profit from which he must deduct the premium (100*25€ - 100*20€) - (premium 200€) = 300€ profit. He can sell his call to close his position or exercise the option to buy 100 shares at 20€.

This example indeed shows that the buyer's maximum risk is limited to the premium.

The seller

For the seller, the risk is different:

![]() If the option is "out-of-the-money", the seller earns the premium and doesn't have to buy the shares, since the buyer is not going to exercise his right.

If the option is "out-of-the-money", the seller earns the premium and doesn't have to buy the shares, since the buyer is not going to exercise his right.

![]() If the option is "at-the-money", the seller earns the premium if the buyer doesn't exercise his option.

If the option is "at-the-money", the seller earns the premium if the buyer doesn't exercise his option.

![]() If the option is "in-the-money" and the buyer exercises his option, the seller must buy the 100 shares at the 25€ exercise price even though the market price is 20€. He therefore loses (100*25€) - (100*20€) + (premium 200€) = -300€.

If the option is "in-the-money" and the buyer exercises his option, the seller must buy the 100 shares at the 25€ exercise price even though the market price is 20€. He therefore loses (100*25€) - (100*20€) + (premium 200€) = -300€.

The seller's profit is therefore limited to the amount of the premium and his potential for loss is unlimited.

A hedging tool (Purchase of a PUT)

Options are particularly effective to protect a stock portfolio against a decline in the stock markets.

Buying a PUT guarantees a selling price for the investor. If stock prices drop, he will be able to sell his shares above market prices.

In the event that stock prices rise, the investor can elect to not exercise his put options, he will simply lose the premium paid to purchase these options.

Buying a put option is like buying insurance against the depreciation of one's securities, and the cost of this insurance is limited to the price of the premium.

| Previous: Options trading strategies | Next: Binary options |