You are not logged in.

Pages: 1

- Index

- » Analyses / Forecasts (by major banks and brokers)

- » EUR/USD: why is the dollar currently over-sold?

#1 17-02-2021 10:09:16

- johnedward

- Admin & Trader

- From: Paris - France

- Registered: 21-12-2009

- Posts: 3861

- Website

EUR/USD: why is the dollar currently over-sold?

EUR/USD: why is the dollar currently over-sold?

One of the biggest consequences on the financial markets is the weakening of the US dollar. It weakened last year, and it will weaken in the future. The arguments for this are more than convincing: the United States is the country with the most aggressive monetary and fiscal policy in the world.

Looking at the fiscal package, the U.S. stimulus amounts to nearly $3 trillion - $900 billion from last December, which will make its way into the economy this year, and an additional $1.8 trillion expected to be provided by the Biden government by the end of this February.

However, some caution is called for. Yes, the much-needed fiscal stimulus is weighing on the dollar's strength, but a comparison with what is happening in other parts of the world is prompting the prudent investor to at least rethink the weaker dollar thesis.

A strong economic recovery bodes well for the greenback

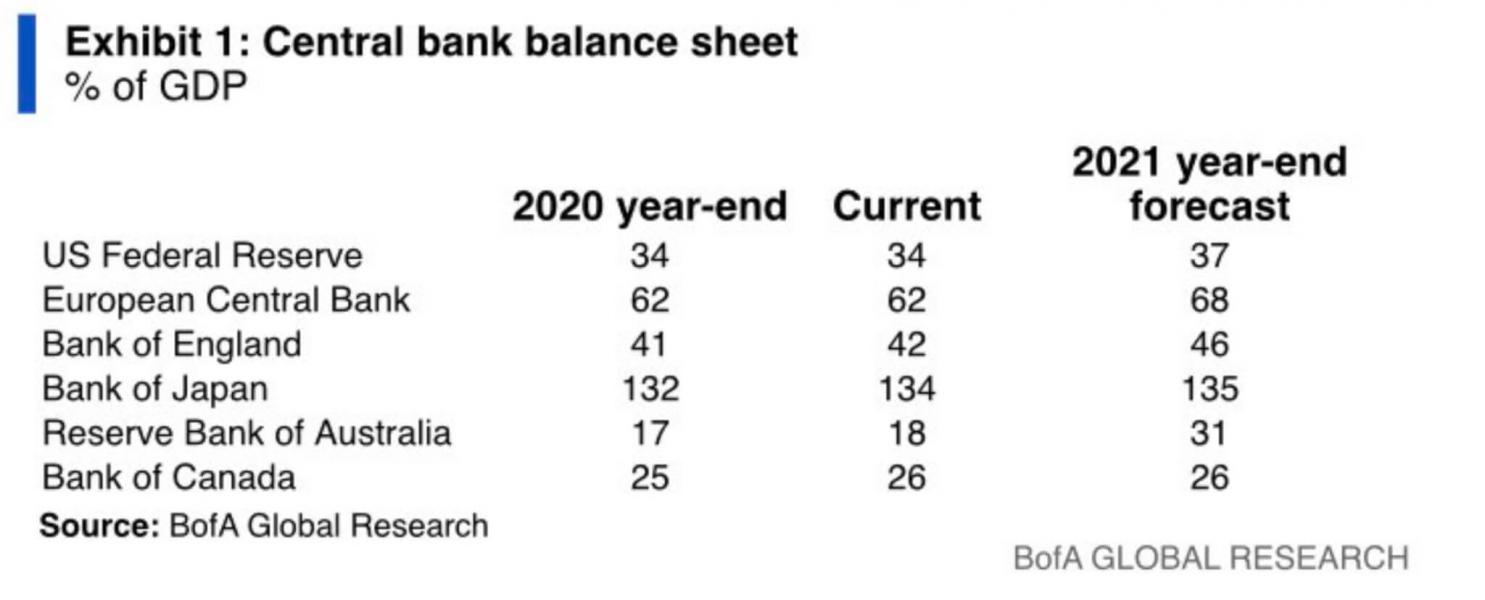

Dollar bulls, however few in number, have three arguments for the return of the greenback. The first is the balance sheet of the central banks.

The picture above reflects an incredible but simple aspect: the Fed's balance sheet is not the "largest" in the world, as many would have thought. After the great financial crisis of 2008 and the introduction of quantitative easing (QE), it is central bank balance sheets that need to be examined in order to estimate the conditions of accommodation in an economy.

How can this best be done other than by comparing the balance sheet to the size of the economy? Therefore, the central bank's balance sheet as a percentage of gross domestic product (GDP) is a key measure for understanding the effect of quantitative easing on individual economies and, therefore, for applying the result when searching for fundamental trades in the foreign exchange market.

The Fed is NOT the central bank that offers the most accommodative conditions. The Bank of Japan, the European Central Bank, the Bank of England - they all have larger balance sheet expansion when measured as a percentage of GDP.

Second, the vaccine rate. The United States leads the world by two points - almost a million people are vaccined every day. At this rate, which tends to increase, herd immunity is within reach (around the end of the summer) - which brings us to the third argument.

Greater fiscal stimulus, combined with an increase in the pace of vaccination, will allow for a faster economic recovery and, why not, higher growth, even compared to pre-pandemic levels. Indeed, this means that the Fed's balance sheet will shrink, rather than grow, as the economy is growing faster than its competitors while EQ is still measured as a percentage of GDP.

Dollar bears can take advantage of the current environment, but conditions may not last long - the faster the US economy rebounds, the less impressive the Fed's quantitative easing will be.

"Anything worth having is worth going for - all the way." - J.R. Ewing

Offline

Pages: 1

- Index

- » Analyses / Forecasts (by major banks and brokers)

- » EUR/USD: why is the dollar currently over-sold?