You are not logged in.

Pages: 1

- Index

- » Analyses / Forecasts (by major banks and brokers)

- » EUR/USD: quantitative easing at heart of USD strength

#1 06-10-2021 08:59:28

- johnedward

- Admin & Trader

- From: Paris - France

- Registered: 21-12-2009

- Posts: 3861

- Website

EUR/USD: quantitative easing at heart of USD strength

EUR/USD: quantitative easing at heart of USD strength

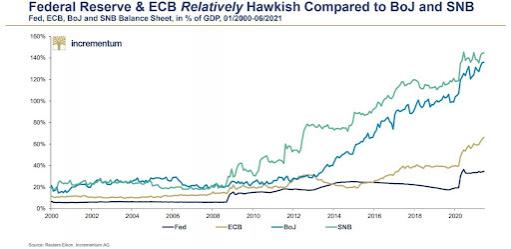

Unconventional monetary policies have led to huge differences in the balance sheets of central banks. The balance sheet expansion of the ECB and the Federal Reserve is nothing like that of the Bank of Japan or the Swiss National Bank.

The dominant theme in the currency market in 2021 is the strengthening of the USD. Also known as the "greenback", it has gained ground on its peers, as evidenced by the EUR/USD exchange rate, which has risen from 1.23 to 1.16, or the USD/JPY rate, which has risen sharply from its yearly lows in the 103 area.

Since the great financial crisis of 2008, central banks have embarked on a new monetary policy model. Until then, we could talk about conventional or traditional monetary policy decisions, where central banks raised or lowered interest rates in response to the strength or weakness of the economy.

But this changed abruptly as a result of the crisis. The US FED started buying government bonds with newly created money. This process, known as quantitative easing (QE), was quickly adopted by other central banks in the developed world and represents an unconventional way of further easing financial conditions beyond simply cutting rates.

The BOJ and SNB have eased policy over the years

Central banks have expanded their balance sheets (i.e. the assets they hold) by buying their own government bonds or debt. With interest rates close to or below zero, balance sheet size and expansion quickly became a measure to compare the aggressiveness of a central bank's loose monetary policy. It is therefore a way to compare (and trade) different currencies.

If we compare the balance sheets of the European Central Bank, the Fed, the Swiss National Bank (SNB) and the Bank of Japan (BOJ), and interpret them as a percentage of GDP, we find that the Fed's easing is not so aggressive. In fact, the Fed's balance sheet expansion is being held back by the faster rate of GDP growth.

Using this metric, it becomes clear that the strength of the US dollar in 2021 is justified, despite the fact that the Fed is still buying US government bonds. Furthermore, now that the tapering of asset purchases is all but announced, the US dollar rally could continue into the final trading months of the year.

Translated with www.DeepL.com/Translator (free version)

"Anything worth having is worth going for - all the way." - J.R. Ewing

Offline

Pages: 1

- Index

- » Analyses / Forecasts (by major banks and brokers)

- » EUR/USD: quantitative easing at heart of USD strength